Contact: data@mbaks.com

January Builders Bulletin: Housing Inventory in King and Snohomish Counties Remains Low

Despite Increase

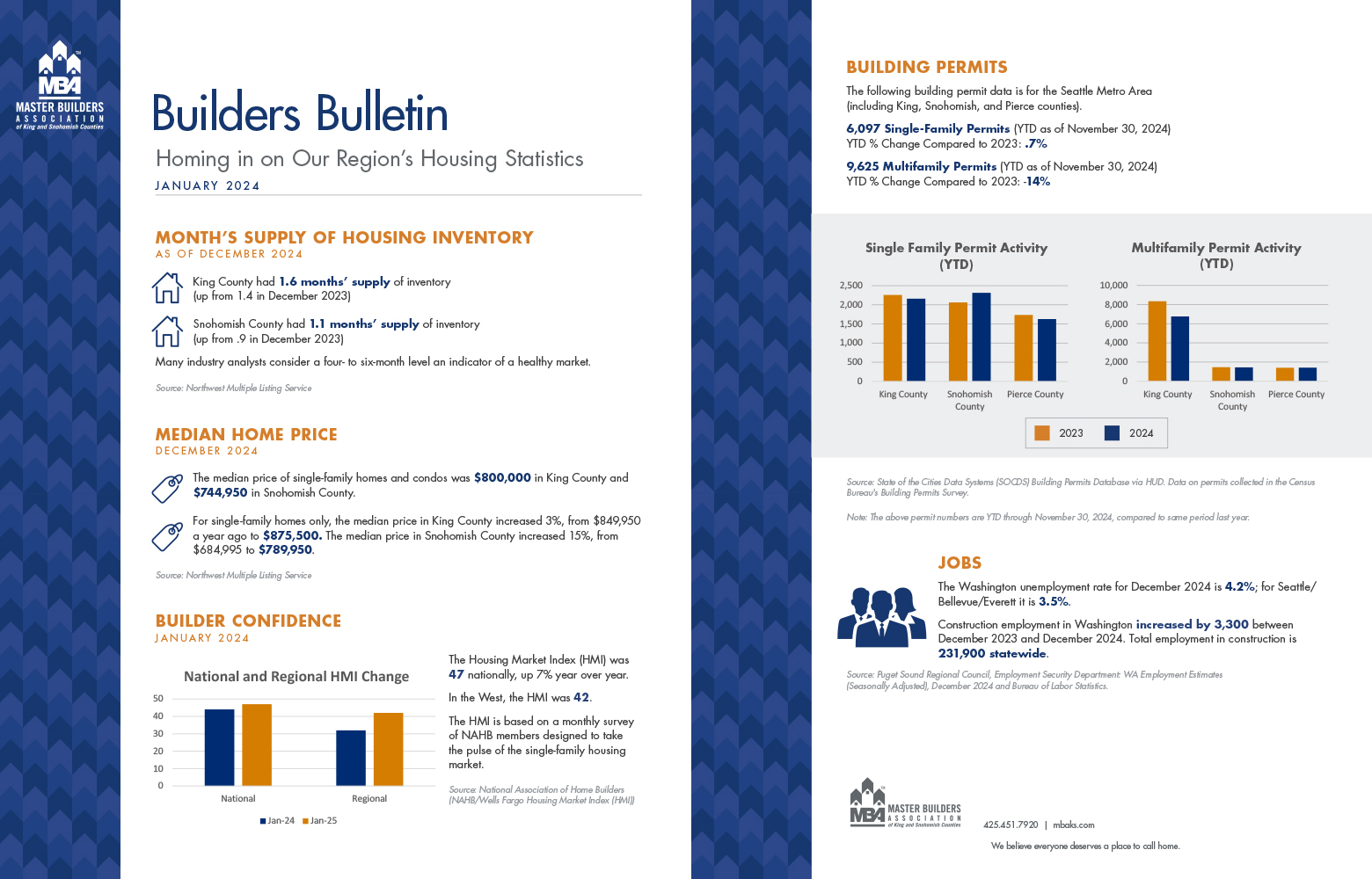

As of December 2024, the housing inventory in King County stood at 1.6 months’ supply, a slight increase from 1.4 months in December 2023. Similarly, Snohomish County experienced a rise in housing inventory, reaching 1.1 months’ supply, up from .9 months the previous year. While these numbers reflect a modest improvement, they remain well below the four- to six-month supply level that many industry analysts consider indicative of a healthy market.

READ THE FULL REPORT

january-builders-bulletin